A Kind of Neither Keynesian Nor Neoclassical Model (6): The Ending State of Economic Growth ()

1. Preface

Lucas has been attracted by the questions on economic growth: “Is there some action a government of India could take that would lead the Indian economy to grow like Indonesia’s or Egypt’s? … Once one starts to think about them, it is hard to think about anything else”. [1] While it may be necessary to swap out the role, Lucas’s question still has important theoretical and practical significance before figuring out whether economic growth is endogenous or exogenous.

Unlike the economics of the Adam Smith era, modern economics, which is close to various labels, is not content with the literary logic of explaining economic phenomena. However, more use of the mathematical logic does not guarantee that the analysis results are better than the literary logic. The advantage of mathematical logic is that it is easier to find bugs in the process of reasoning, and that problems such as preconditions, variable settings, and implicit conditions are even worse than literary logic. Dynamic Stochastic General Equilibrium (DSGE) has been used for economic problems extensively since the 1960s, and the Keynesian and Neoclassical schools have used it to demonstrate their theory. Of course, we can also use it in our model. What will happen?

2. Dynamic Optimization Analysis on Condition

or

In the Solow model, output growth depends on capital growth, capital growth is a function of net investment, and net investment is part of the output, which can use the mathematical tool of DSGE to analyze the time path and the ending state of the output changes. In the dynamic analysis of the utility function of consumption, we do not know the specific form of the utility function, but as long as the utility function is convergent and satisfies some constraints, we can get some important results according to the standard solution of the dynamic maximum principle.

The study of Cass shows that assume the utility function of per capita consumption

at a certain time satisfies the condition

,

,

,

, and the Solow

model

is used as the transfer equation (among them

) in the dynamic optimization, then the shadow price

of k, the time path of the per capita consumption c and the capital k can be solved according to the Pontryagin maximum principle. The results have no difference from the original Solow model [2] .

However, our study shows

. If the constraint condition

in Solow model is replaced by

(where

) [3] , then we need to re-verify the following three conditions of the Hamilton function in the dynamic maximum principle:

(1)

(2)

(3)

Let

(where N is the labor population), substituting it into the identity

, and the following transfer equation is obtained from

[3] :

(4)

If the objective function is assumed to be the maximum utility of per capita consumption as the dynamic model of Cass, its dynamic optimization problem is as follows:

(5)

The corresponding Hamilton function is:

(6)

Among them,

is the per capita consumption, the discount rate r in

is assumed to be the market interest rate, λ is the costate variable,

is the per capita capital,

is the growth rate of labor force. The Hamilton function is differentiated for c and k respectively:

(7)

(8)

According to the necessary condition shown by Equation (2)

,

(9)

In the above equation, the discount factor

is not 0 at time t, so we can only make

. This means that the utility

is a constant greater than 0. Therefore, the first part of the Hamilton function

is not 0 when

. From the necessary condition shown by Equation (3)

,

(10)

where r and n are exogenous variables and assume that the rate of population growth n is less than the market interest rate r, that is,

, the general solution of Equation (10):

(11)

From the transfer equation

, the general solution of k is:

(12)

Then, the Equation (11) (12) is brought into the second part

in the Hamilton function,

It is shown that unless

in the Hamilton func-

tion

, otherwise

. It is not possible to satisfy the neces-

sary conditions shown in Equation (1). Equation (9) shows that the consumption utility

is a constant and

, so

cannot be established.

The reason for this is that

is decreasing in the transfer equation

of the Solow model, but

is not diminish when the increase of k in our transfer equation

.

We can also construct dynamic models in another way. Since

and Y are already present in our basic equation

[3] , there is no need to introduce the labor population N in order to convert Y and C to per capita output y and consumption c as the dynamic model of Cass. We directly use the total consumption C in the utility function, the dynamic optimization problem can be simplified as:

(13)

The corresponding Hamilton function is:

(14)

(15)

(16)

According to the necessary conditions

and the Equation (15),

(17)

Since we do not know the specific form of the utility function

, the limit of the costate variable

can not be determined by Equation (17). From the necessary conditions shown in Equations (16) and (3),

(18)

Since r in Equation (18) is an exogenous variable greater than 0, we can get the general solution of

:

(19)

(20)

Equation (20) can not guarantee

, because the function

also contains the variable Y, we need to examine the changes in Y. According to the transfer equation

, the general solution of Y is:

(21)

From the Equation (19) and (21),

Therefore, unless

, otherwise

. In the economic

sense, the utility

should not be less than 0 (if utility less than 0 the con-

sumption is meaningless), it is,

, so there is no

.

1There are three types of variables in the macroeconomic analysis: incremental, stock, and mixed. In a closed economic system that ignores foreign trade, the statistical identity of the output is expressed as

, where C is consumption,

is the gross investment, I is the net investment, and D is depreciation. Exactly, there is a theoretical bug in this identity. Assuming that the output of this period (t) is

and the output of the previous period (t − 1) is

, the exact identity should be expressed as follows:

. Therefore, in the identity,

,

,

and

are incremental variables,

,

and

are stock variables,

,

and

should be called the amount of mixing because

both incremental and stock variable. Since I is the increment rather than the stock, theoretically it can only appear in the incremental expression:

.

In the Solow model, since

,

is bounded by the assump-

tion of

. Therefore, the limit of the first term in the Hamilton function is always 0; the second term consists of the costate variable

and the transfer equation

. The effect of c and δ on the

in the transfer equation is negative and the margin of y is decreasing, so the limit of the second term of the Hamilton function is also 0.

When the transfer equation is changed to our

or

, the consumption and the depreciation do not restrict the growth of K and Y because

has already includes increased consumption and depreciation. If the fluctuation of output in short-term are ignored, the output growth rate

is independent of the size of K and Y at any time (including

), only by the marginal state variable r. As long as

,

or

will not be 0, so the limit of Hamilton function can not be 0 and the transversality condition

can not be satisfied. The model of per capita variables, which considers the change in the labor force as in the Equation (5), is no exception.

From the Cobb-Douglas function

,

, let

, then

. Assuming that

and r are independent of K and Y changes (we will see that the assumption is reasonable from the equation

), then

, and then by the statistical identity

1,

In the Cobb-Douglas function, C and I are not the cause of the change in output, but the result. Since the investment and depreciation increment is only part of the output increment,

is always less than

, and because of

,

, the investment is much smaller than the capital increase. Therefore, it is impossible to obtain the correct conclusion for all dynamic optimal analysis based on the hypothesis of

.

The statistics show that about 80% of the newly increased output

is used for the newly increased consumption

. In the above equation because

, so

, I is only a small part of

.

is not unreasonable in reality. Because net investment I in addition to generating equal assets with I, but also bring the production technology upgrades, improve production efficiency and other non-physical assets changes, it is these changes make greedy investors willing to take possible risks.

3. Exogenous and Endogenous Growth

Assuming L in

as a labor population can give us a benefit that simplifies

to a formal univariate function

, where

, N is the labor population. Full differential of

:

(22)

Assuming that

and A are constant,

(23)

If

is further assumed, then

, where

is the gross investment and

is the depreciation rate. By the identity

,

, the growth rate of population

, then

(24)

Among them,

. Assuming that the consumption rate

, then

. Obviously, the savings rate s is determined by the consumption rate c. Substituting Equation (24) into Equation (23):

(25)

The Equation (23) and (24) show that since the marginal output of k decreases, the contribution of k to

is getting smaller and smaller, and the depreciation

grows linearly with k increases. Therefore, regardless of the current state of growth of the economic system, even if the population growth rate n is 0, the economic system can not avoid the end state, that is,

. For a finite time, when k grows to

, or

, the net capital growth will be lost to the depreciation of capital stock. Thus, even if people do not consume at all, output all for investment (

), it can only extend the time that the output growth rate is reduced to 0.

To make

in the Solow model not diminish, a simple improvement is to think of the A in the Cobb-Douglas function as a variable that grows with k. The Equation (23) shows that there is

as long as

, or

. people generally believed that A is the technical condition in the production process, is exogenous factor and does not adjust automatically with k changes. Therefore, the Solow model is considered a kind of “exogenous growth theory”.

In the subsequent “endogenous growth theory”, someone direct assumptions that the production function is the marginal output does not the diminish functions [4] [5] [6] , another one derived such equations by re-assuming the meaning of the production factor L.

In fact, the A as a constant or that it is an exogenous variable, but people’s subjective assumptions. By

,

(26)

Let

, when

,

,

(27)

Assume

, then

(28)

Since

, so we can have:

(29)

This shows that A is closely related to the marginal state of the production r and the distribution state (

) of the production factors and should be a comprehensive variable that is affected by various factors in the Cobb-Douglas function.

The Equation (28) is obtained at the hypothesis

, and

is not necessary to analyze the per capita output level y. Without assuming

, the per capita output should be expressed as:

(30)

Among them,

(31)

When

, the size of A is related to the size of N and L, except for r,

and k. Therefore, suppose

,we can transform the Cobb-Douglas function into a simple function

for easy analysis, but also confuse the difference between per capita output and hypothesis

.

If L is human resource and let

, E is the coefficient of worker quality

, then the production function is

. If E is a constant, this assumption is not substantially different from the Solow model and the diminishing of output growth rate can not be changed.

Like the “Learning by doing model” [7] , if the quality of human resources is considered to grow with the capital, that is,

, then

, the corresponding production function is

. This is free from the impact of diminishing marginal output of capital with output growth, and the growth of population N not only does not impede per capita output growth as the Solow model, but also promote the growth of per capita output.

If

, then

, so

, or

. This is called the “AK model” and is the most concise endogenous growth model [5] [6] .

Note that there is no A as an endogenous variable in the above-mentioned production function, which derived from the various assumptions about human resource L above. If A is regarded as an endogenous variable and is substituted into the “Learning by doing model” and the “AK model”, it is found that there is no essential difference between the two models.

From Equation (31), in the “Learning by doing” model and the “AK” model, the expression of A should be:

“Learning by doing model”:

“AK model”:

They are substituted into the “Learning by doing model”

and the “AK model”

, respectively, the,

“Learning by doing model”:

“AK model”:

It like a game in mathematics. As long as A is regarded as an endogenous variable, all models are nothing but an expression of the equation

. The problem is that when

,

and

can be used to express the relationship between Y and K, but A contains variables associated with r in

.

Lucas discovered the gap between rich and poor countries in capital marginal output in his analysis of Indian data in 1990 [8] . This is called “Lucas’s Paradox”. In fact, if a clear endogenous A, we will understand the so-called “Lucas’s Paradox”. The equation

(from

) is brought into the Cobb- Douglas function

, then

, this is,

(32)

where, r is

. The trap of Equation (32) is that if A is seen as a constant, we can predict the marginal output

by the per capita output of a country.

For example, the per capita output of the United States is 15 times that of India, assuming that

both countries in Equation (32), then India’s marginal output

will be 58 times that of the United States. In such a big gap, American capital should go to India to get amazing benefits, so Lucas said that neoclassical theory simply can not reasonably explain the real world.

However, if the Equation (29)

is brought into Equation (32), we find that Equation (32) is another expression of

. The equation

indicates that the difference in interest rate between the two countries is determined by the difference in output-capital ratio

between the two countries, not determined by the difference in the level of per capita output y. Although the per capita output of the United States is 15 times that of India, if the US per capita capital k is also 15 times that of India, the interest rate (capital marginal output) of the two countries will be very similar (assuming the difference of α between the two countries is not significant). Therefore, although the per capita income of countries may have a big gap, but the interest rate gap is not large (especially the real interest rate).

Lucas said there were several ways to make the economy of India rapidly grow, the first one is to improve the original production efficiency, the second one is to make full use of domestic resources through international trade, the third one is to earn other country’s transfer payments through diplomatic access that have significant effect on its own economy.

The essence of “trade to be rich” is to turn the idle resources of a country into a real income that can improve people’s living standards. If use some revenues from trading to import technologies and to improve the domestic production efficiency, the process of getting rich will be faster and more sustainable. The export of cheap oil in the Middle East, and export of cheap labor in China with the help of “two outsides (products and raw materials), two large (export and import)” are the example of “trade to be rich” in economic globalization.

In theory, as long as the clear

, no matter how the assumption that L can be, it will only cause the formal changes of the production function. For example, assuming that the monetary value of human resources is the income it obtains in the market:

, then

, that is,

.

In the philosophical sense, if the contribution of material resource K to output is also derived from human wisdom, all income is the contribution of human resources, that is, assuming

, then

. Obviously, this hypothesis derived production function has also the characteristics of “Learning by doing model” and the “AK model” that the marginal output does not diminish. Table 1 summarizes the changes in the Cobb-Douglas function under various assumptions of L.

In addition to these assumptions shown in Table 1, we can also think of more reasons to assume more. In short, by assuming a different L and subjective interpretation of L, any desired endogenous growth or exogenous growth model can be obtained. However, as long as the corresponding change of

and A is introduced, all models are not different, and are the deformation of the marginal state equation

or

of the Cobb-Douglas function. Equation

is not only the starting point for the analysis of the cyclical changes in output [9] , but also implies the output growth path and the

![]()

Table 1. The influence in the various hypotheses of L on the Cobb-Douglas function and the parameter A.

final state of the information.

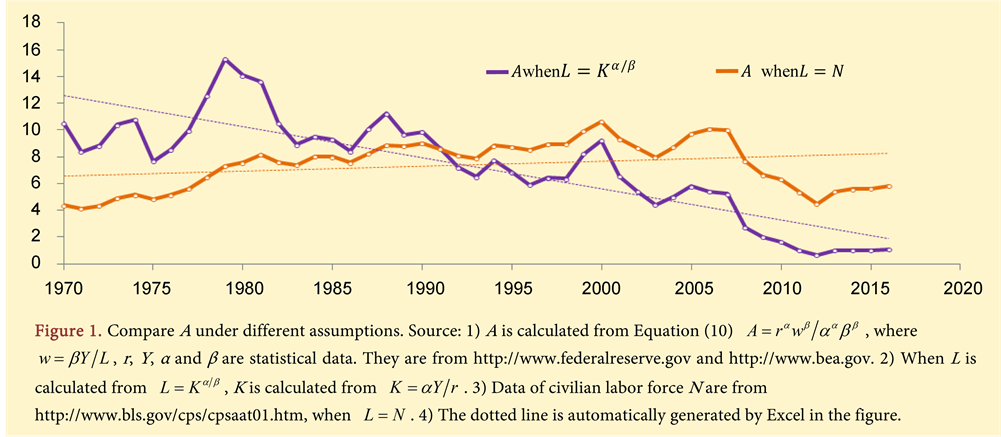

Figure 1 shows the difference in A assuming

and

. Under the assumption of

), the change of A is obviously decreasing, and in the other way, A shows a slight upward trend. Therefore, A is the variable associated with the hypothesis L, not a constant.

Gollop and others on the statistical analysis think that the contribution of capital is the first, the labor force is second, and the contribution of the productivity is less than one quarter in the economic growth of the United States [10] .

After the Cobb-Douglas function

is fully differentiated, the

in Equation (33) is called Total Factor Productivity (TFP).

(33)

Since the sum of

and

is less than

in the statistical data, It is believed that the residual

is the contribution of technological progress. If L is determined by

, the average of

will be negative (during 1970-2016, the average value of

is −0.0268). Because A decreases with output (see Figure 1). This difference is due to the fact that Gollop’s estimates do not take into account the marginal relationship between the variables in the Cobb-Douglas function. If the marginal equation

is fully different,

(34)

Substituting Equation (34) into Equation (33), according to

and

,

(35)

In Equation (35), the first term shows that

is also affected by

and

, the second term

is the fluctuating variable that causes r periodic change, and the third term

is increased and fluctuates periodically

in the statistical data. It would be easier to understand the nature of A by rewriting the Equation (27)as follows:

where r and w are the marginal states of K and L, and the function of α and β is the effect-proportion of r and w in the production. In this way, A is an endogenous variable that contributes to the marginal contribution of factors K and L with the distribution parameters α and β. It plays an important role as bridge in the Cobb-Douglas function

and the marginal state equation

. Ignoring the endogeneity of A ignores the relation between

and

.

4. The Final State of Economic Growth

According to “A Kind of Neither Keynesian Nor Neoclassical Model (5): The Path of Economic Growth” [11] we know that regardless the production state of the system is

(on the left side of the Cobb-Douglas function bisector

), or

(on the right side of the Cobb-Douglas function bisector

), the state will close to the bisector

driven by market competition. And the state of limit is

, namely

, at that point

. Therefore the final state of variable A is:

(36)

In Cobb-Douglas function

, because

[9] , when

,

, therefore,

(37)

This is the result of the “AK model” or the “Learning by doing model”: the contribution of K to the growth of output is not marginally diminishing. The “AK model” and “Learning by doing model” are derived from the subjective interpretation of L, and our endogenous model is derived from the final state of A and Y.

Equation (37) shows that the final state of output Y is still a function but not a constant. In the final state function

, the relation between Y and K evolves from an exponential relationship of

to a linear relationship, and the output growth does not terminate due to the growth of K.

Differentiate

, then

. In the final state,

only has the second item in Equation (35). This shows that A will fluctuate due to the fluctuation of r (r fluctuation reasons see reference [9] ).

It is simpler to derive the final state of the output Y from the marginal state equation

of the Cobb-Douglas function. Since

when

,

(38)

Comparing Equations (37) and (38),

and

are the equivalent expression of Cobb-Douglas function. From the equation

we can see that when r is an exogenous variable,

. This suggests that “the marginal output of production factors is decreasing” is a relative definition. When the marginal output of all factors in production is equal to each other, the output increment

is not necessarily diminishing compared to the factor increment

, since the increment of another factor

also contributes the same to

.

Microeconomics divides production into three states. In the first, the marginal output of K is greater than the average output (

). In the second,

, the third is the inefficient state, because

. In the macroeconomic field, since the marginal output

, the average output of K

,

, so

. This suggests that, as long as

, the production in the macroscopic sense is always in the second state of efficiency.

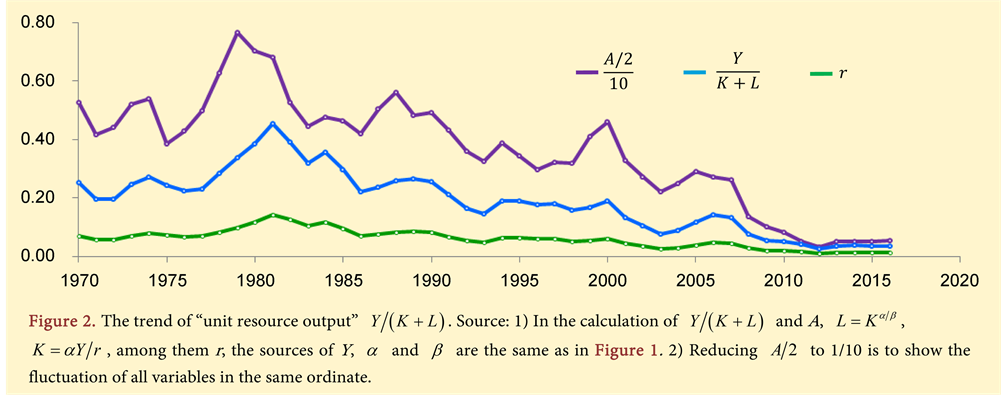

We have defined

as “unit capital output” [11] , and now its economic significance is more obvious. Since

,

, when

,

,

, then,

(39)

“Unit Resource Output”

is actually “Total Factor Average Product (TFAP)”. At

, TFAP is always greater than the marginal output

or

. As the output Y grows and

, the TFAP will become more optimized [11] and will be close to the marginal output

or

.

According to statistical data of the United States, as shown in Figure 2, there are always

. And based on Equation (36) and (39), we can get the following inequality, where the equation is satisfied when

.

(40)

As in the case of traditional theory, it is impossible to have the above inequality if L is the labor force N. The most straightforward reason is that there is no comparability between A,

and r, because their dimensions are inconsistent. For example, when L is the employment population, the dimension of thousands of people, What is the dimension of A and

?

The final state of the production function does not mean that the output growth will eventually stop. Differentiated the final state equation

, then:

(41)

This is not contradictible to the fully differential equation of

, since

is not the final state, so

. In the final state

, so

. From the basic equation

[3] , then

(42)

This is the cycle equation of the growth of output that we have previously derived [9] , but at that time we assumed that in the short term

. Therefore, although the final state production function

is different from the production function

or

, the factors that determine the core output growth rate in short-, medium- and long-term are the same, which is the core interest rate

. And as long as the core interest rate

is greater than 0, Even if the production function evolves to

, the business cycle will not disappear.

If we neglect the periodic fluctuations in output growth, then

. Rewrite it as a differential equation varies along time

, the general solution is:

(43)

Although this time path function of Y does not have abundant production state information as the Cobb-Douglas function, it is not like

, when

, the result is not understandable:

. For the time path function

, when

, then

, the system is in a simple reproduction state.

The Harrod-Domar model assumes that the production function is

[12] [13] . This can be seen as a simplified form of the marginal state equation

expressed. Although the subsidiary hypothesis

is not correct, when introduce coefficient b in

, then

. And with the production function

, then

. According to the statistical data, I is a part of the output

, assuming

, where s is another coefficient that is different from b (note: we do not call s for the savings rate), so

. Rewrite it as the differential equation considering time

, then its solution is

. As long as the coefficient (abs) is regards as the interest rate r, there is no difference with Equation (43). Therefore, regardless of whether the analysis of Harrod-Domar model is correct, the time path of its output is roughly the same as our conclusion.

The Solow model uses

as the production function and regards A as a constant. Although the auxiliary assumptions

and

are the same as those of the Harrod-Domar model, the output will finally stop increase in a limited time since the growth of output is constrained by dual factors of the “diminishing capital marginal contribution per capita” and “stock capital depreciation” [14] .

Comparing Equations (41) and (34), it can be seen that the difference between the growth rate of the final state and the short-term is that there is less (

) in Equation (41). The average number of

in the United States from 1970 to 2016 is 0.0070, so before the Cobb-Douglas function evolves to the final state equation

, the real output growth rate

for the removal of the inflation rate should be slightly reduced.

of the United States increased from 0.2770 in 1970 to 0.3691 in 2016, and experienced an annual growth of about 0.00196 for 47 years. Assuming a linear increase at this rate, after another 71 years,

in the United States will reach 1/2. As the theoretical growth rate of

is decreasing, so in 2087 we may not see the actual value of

equal to 1/2.

Since α is not a variable that determines whether the marginal output is greater than zero or not, the growth of output is determined by the interest rate r in the production function

or

. The speed of output growth is not the production function itself, but on the production efficiency.

Adam Smith said in An Inquiry into the Nature and Causes of the Wealth of Nations that there was an “invisible hand” that led self-interest people promoted public interest [15] , but Smith had never revealed the metaphor in the book. Some people say “invisible hand” is the relationship between supply and demand, some said that it is the market price, and some said that it is market competition, and so on. We believe that “invisible hand” means “market competition”. Market competition raises the production efficiency and makes it necessary for producers to return the surplus generated by the increase of efficiency to the society.

During 1970-2016, the average of real interest rate in the United States

is 0.0229. Assuming that the number can last 200 years, the actual output

will also increase at the average annual rate of 0.0229. Then after another 200 years in year 2216, the actual GDP will be 92.61 times the current GDP. According to the annual population growth rate 0.010 of the United States in 1970-2016, by 2216 the total population will be 7.32 times the current. At that time, the real per capita GDP in the United States would be 12.65 times that of 2016, or per capita GDP of 651,684 USD (real GDP in 2016 is 16,660 billion USD, 323,391 thousands population, 51,517 USD/person).

The question is with the income level of up to real 650,000 USD/person, will people be involved in the exhausting competition for higher income? Perhaps when it has not yet reached this figure, many people have already voted for the party who advocates for the universal welfare policy. Therefore, the terminator of economic growth is not the Cobb-Douglas production function, but at what level of income, those who believe in “market competition” will become social minorities.

5. Conclusions

The issues we are concerned with today are not much different from what Adam Smith was concerned about in his great work of two hundred years ago, but at that time most of the research methods were empirical and conjecture, and we now have to use strict analytical methods and data validation. Our model is derived from the Cobb-Douglas function, and only

will have

,

is determined by the marginal state of real production and inflation, so we conclude that the equation of growth is endogenous, the cause of growth is exogenous.

No matter the growth of output is generated by the economic system revolution, the improvement of production management or the progress of science and technology, ultimately the result is the increase of production efficiency. These are in the model that the marginal output is greater than 0. So, regardless of

![]()

Table 2. Summary of macroeconomic model based on Cobb-Douglas function.

whether the ending state of

is

, as long as the marginal state of production is greater than 0, Adam Smith said “The Wealth of Nations” will continue to grow.

The 2008 financial crisis made the fabulous former Federal Reserve Chairman Alan Greenspan into a nude swimmer and humiliated the once brilliant traditional macroeconomic theory, but the textbooks still propagate those misleading theories. We abandon the traditional analytical framework, trying to use axiomatic methods to derive the various models of macroeconomic problems, thus forming a new system of macroeconomics with an interest rate as the core variable. Table 2 summarizes these models and helps us understand the link between economic growth and other macroeconomic problems.

Compared with the traditional theory, these models are not only very rigorous in theory, but also have the important practical significance: Based on these models, we will identify the characteristics and causes of the financial crisis, and make a contribution to the prediction or avoiding the next financial crisis.